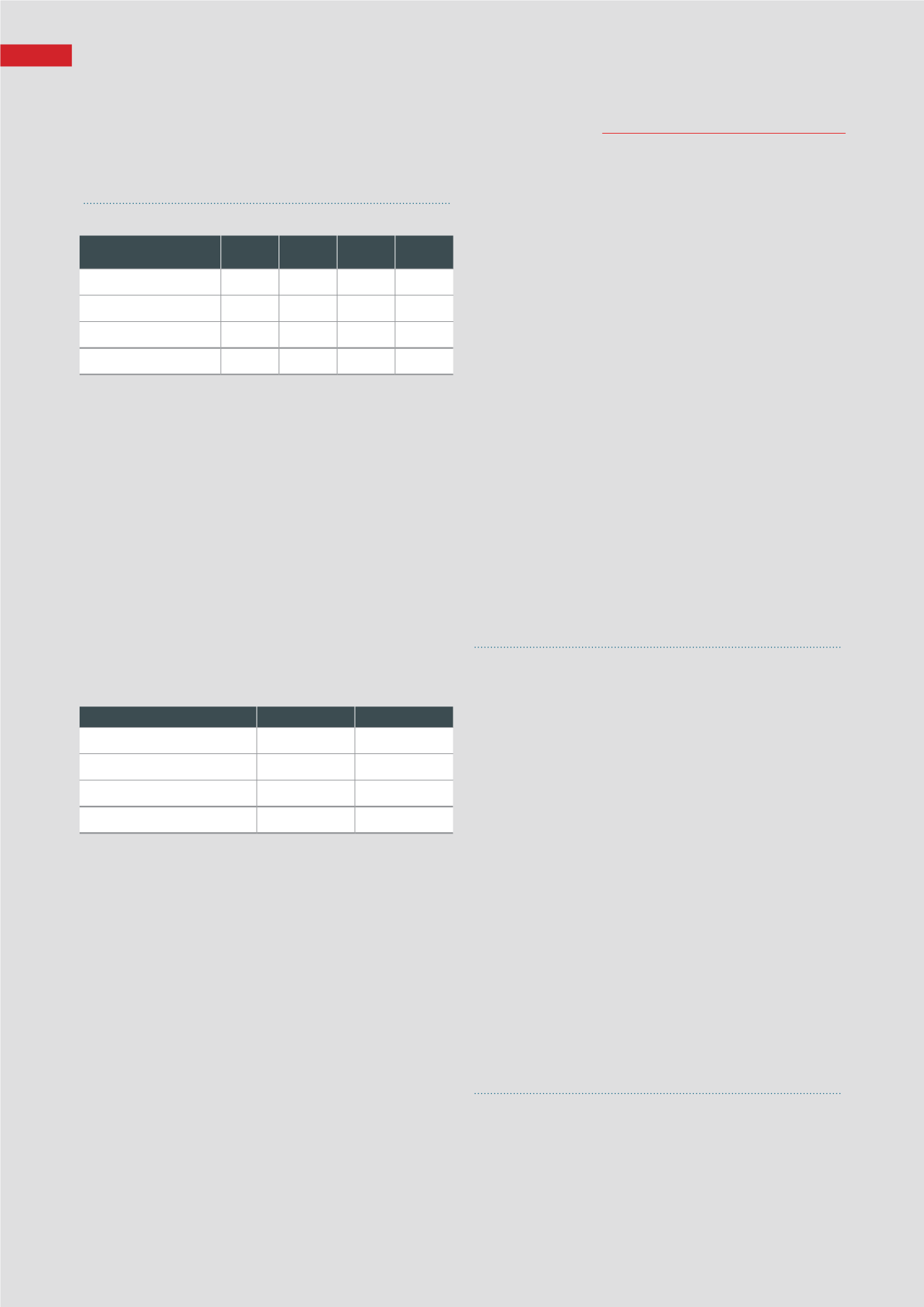

REVENUE AND EARNINGS

Revenue (external sales)

Gross Profit

In $’ million

FY 2014

% FY 2013

restated

%

Civil Engineering

57.4 21.9

76.5 88.2

Properties Development

193.5

74.0

-

-

Properties Investment

10.7

4.1

10.2

11.8

261.6 100.0 86.7 100.0

In $’ million

FY 2014

FY 2013 restated

Civil Engineering

37.5

29.7

Properties Development

52.6

-

Properties Investment

7.4

7.1

97.5

36.8

Revenue increased by $174.9 million (201.8%) to $261.6 million

for the financial year ended 31 December 2014, mainly due to the

recognition of revenue from the industrial development property

project, Ark@Gambas, which obtained TOP in November 2014. In

line with the adoption of INT FRS 115, revenue and related costs

for industrial development project is recognized on completion of

project. As at 31 December 2014, about 87% of Net saleable area

was sold for Ark@Gambas. The civil engineering segment revenue

was $19.1 million lower due to the substantial completion of the

Marina Coastal Expressway project and the two new projects that

was awarded in 2014 and just commenced construction activities.

The revenue from Properties investment segment were mainly

rental income from workers dormitory, which was marginally

higher by $0.5 million to $10.7 million.

Gross profit increased by $60.9 million (164.9%) to $97.5 million

for the current financial year mainly due to the recognition of the

Ark@Gambas project of $52.6 million and the increase of $9.8

million of civil engineering segment due to the finalization of

account for the completed projects and the construction profit

for Ark@Gambas recognized in tantum with tthe inter company

construction project. The gross profit for workers dormitory

remained stable.

Other income increased by $0.4 million to $2.6 million mainly due

to a one time bond early redemption fee of $0.2 million and higher

interest income of $0.2 million.

Distribution cost was $0.2 million higher as the agent commission

cost for Ark@Gambas was recognized in line with the sales

recognition.

Administrative expenses was $2.8 million (66.3%) higher than

previous year mainly due to the higher performance bonus accrued

and higher staff cost and bonus for 2014.

The decrease in the fair value of investment properties was

related to the impairment of the workers’ dormitory. The workers

dormitory is stated at fair value determined on the discounted cash

flow method provided by an independent valuer and the fair value

is expected to be $4.3 million lower with the projection of cash

inflow reduced over the lease period. The lease is expiring at end

of 2015.

The fair value of the investment securities was adjusted downward

by $0.2 million in accordance with the market price of the quoted

shares market value as at end of 31 December 2014.

With the revised FRS 28 and FRS 111, the Joint venture project

for the Dairy Farm Project, the Skywoods, is accounted for using

the equity method, and the share of profit for the current financial

year was $0.04 million compared to share of loss of $1.8 million

in FY2013. Previously this joint venture is accounted for using

proportionate consolidation.

Profit before taxation increased by $58.1 million to $87.4 million,

resulting mainly from the higher revenue and gross profit.

FINANCIAL POSITION

The Group’s non-current assets was $10.5 million higher as at 31

December 2014 was mainly due to the acquisition of the held –to-

maturities security of $7.6 million and higher deferred tax assets

of $6.7 million offset by decrease in investment property by $4.3

million due to the fair value adjustment of the worker dormitory.

The Group’s current assets increased by $10.9 million to $355.2

million. This was mainly due to the higher cash and short term

deposit of $62.7 million and higher trade receivable of $27.0

million, also higher prepayment of $7.5 million for the advance

payment for the Tuas site, offset by the lower development

properties of $84.4 million due to the cost recognition of Ark@

Gambas.

The Group’s current liabilities decreased by $5.7 million to

$193.0 million. This was mainly due to the lower progress

billings to customers and progress billings in excess of

work-in-progress with the recognition for completed projects,

offset by the higher provision for tax and project defect and

warranty cost for completed projects. The remaining bank loan of

$5.0 million was reclassified as current.

CASH FLOW

Net increase of cash and short term deposits of $62.7 million

for FY2014 was mainly due to cash generated from operating

activities arising from TOP of Ark@Gambas project, advance

from Maxwell station project, which was partially offset by the

dividend payment, acquisition of held-to-maturities security and

repayment of bank loans.

OPERATIONS AND FINANCIAL REVIEW

Hock Lian Seng Holdings Limited

Annual report 2014

8